The debate between term and whole life insurance often confuses many families, mainly because the differences between life policies can seem more complex than they actually are. Here's the thing: understanding whole life benefits early helps guide wise choices. The term' insurance cost' also matters when selecting coverage that fits most budgets. When people start comparing these plans, they often turn to life insurance FAQs to clear doubts. What this really means is simple learning that helps choose the best life insurance without guesswork.

Life insurance may seem simple on the surface, but even minor details can make a significant difference. Many folks think both plans work the same, but the truth lies in the life policy differences hidden in each type. Term coverage lasts for a set number of years, while whole life benefits stay active for a lifetime. The confusion usually arises when cost is compared to long-term value. Many families only learn about the differences when they are already picking a plan.

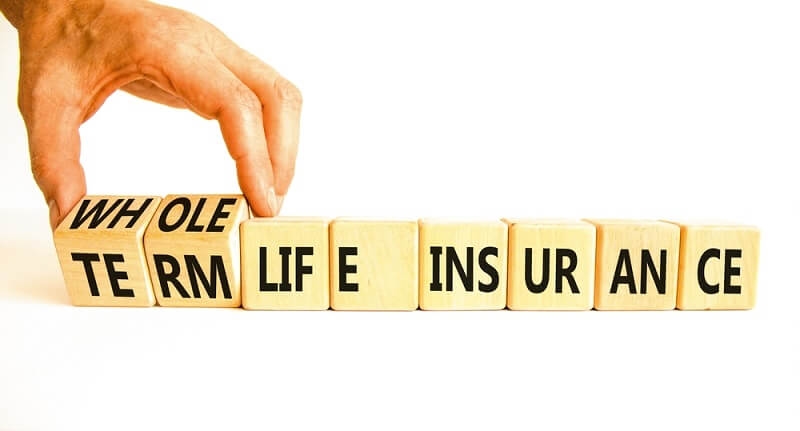

Let’s break it down in a way that feels simple

These pieces shape the complete picture of term vs whole life insurance. Each option fits different needs. Some families prefer lower payments, while others seek lifetime protection.

Term coverage is often chosen first due to financial considerations. Families like having strong coverage without paying too much. The term insurance cost usually stays low because it covers a limited time period. This makes it easier for budget-minded individuals who need protection for their children, homes, or loans. Here's the thing: the lower cost helps families invest extra money elsewhere, which can be beneficial in the long run. This price difference is one of the most noticeable differences in life policies.

Many families choose whole life insurance because it stays with them for their entire lifetime. Entire life benefits include lifelong protection, steady premiums, and cash value growth. The cash value works like a small savings pot that grows slowly but steadily. People sometimes use it later for emergencies, education, or other needs. When plans stay active for life, it gives comfort to families who want no gaps in coverage. Whole life also answers many life insurance FAQs about long-term planning.

A few details help people pick the right plan

What this really means is knowing who depends on the income, how long support is needed, and how much money can be used for premiums. These tiny factors matter more than many expect.

Many questions repeat across families

These life insurance FAQs help people compare life policy differences without stress. When answers feel clear, choosing a plan becomes easier.

Families hold different goals. Some want short-term protection. Some want long-term growth. A few things help decide

The choice depends on goals, not just money. Here's the thing: the right plan saves future stress.

Whole life builds something extra beyond protection. The cash value sits inside the policy and grows slowly. It can be borrowed against if needed. It creates a comfort cushion that term plans cannot offer. These whole-life benefits address many common life insurance questions about future planning and building long-term stability.

Younger individuals prefer the term because premiums are generally lower at younger ages. It helps stretch money while still getting strong coverage. Term insurance cost also helps families buy higher limits for less money. What this really means is creating peace during the years when finances are tight and responsibilities seem overwhelming.

Some families buy term insurance to cover mortgage payments or raise their children. Others buy whole life to leave money behind for future generations. The term vs whole life insurance decision becomes easier when thinking about the future

Seeing needs clearly makes the choice feel natural.

People sometimes make mistakes when choosing without enough info

These questions shape the path to choosing the best life insurance for personal needs. When doubts vanish, confidence grows.

Life never stands still. Jobs change. Families grow—money shifts. A good insurance plan fits these changes. Some people start with a term and later add a whole life to it. Some switch plans when kids grow older. Here's the thing: the important part is checking coverage every few years to see if your needs have changed. This helps match the plan with life’s new responsibilities.

People who want stability often lean toward whole life. Its steady payments and lifetime protection create a strong foundation for long-term plans. Cash value adds extra comfort. The entire life benefits also help families leave a lasting legacy for their loved ones. What this really means is long-term peace built slowly and safely.

Families sometimes start with a term because money feels tight. Later, when finances improve, whole life becomes easier to manage. This blend helps many families handle both protection and growth. Comparing term vs. entire life insurance becomes easier when considering goals instead of just numbers.

A few points stay important

These differences help shape the final decision and make it easier to compare both options.

Choosing between term and whole life insurance becomes easier when you understand the differences in life policies, the benefits of whole life insurance, the cost of term insurance, and answers to common life insurance FAQs. Innovative thinking enables families to select the best life insurance that protects their loved ones and supports long-term plans with clarity.

This content was created by AI